Quick note: this article was last updated on September 24. This article will be updated if there are relevant changes in the future.

Many expats in the UAE, Singapore, Hong Kong and beyond buy life and other kinds of insurance.

Whilst this can make sense, given that you are outside your country’s social security system, are all product offering equal value?

In this article I will be reviewing some of the most widely sold plans in the market, answering some frequently asked questions (FAQs) and suggesting some alternative options available to expats and locals who want international standard coverage.

For people with existing plans, I also suggest what you can do, if you are unhappy.

This article is long. For the time poor and those that want to contact me directly, please email me (adamfayed@hotmail.co.uk or adamfayed@int-amg).

Sometimes I can offer discounts on the online prices you see quoted, depending on the circumstances.

Where are these plans sold?

These plans used to be sold globally. In 2013–2015, however, Zurich and Friends Provident exited many markets.

These days, therefore, they tend to only be sold in 2–4 expats hubs, but there are many people with older plans.

Rl360 LifePlans are sold globally in over 100 countries.

What’s the difference between term insurance and whole of life insurance?

Before reviewing these plans, it is important for us to make a distinction between the two main types of insurance.

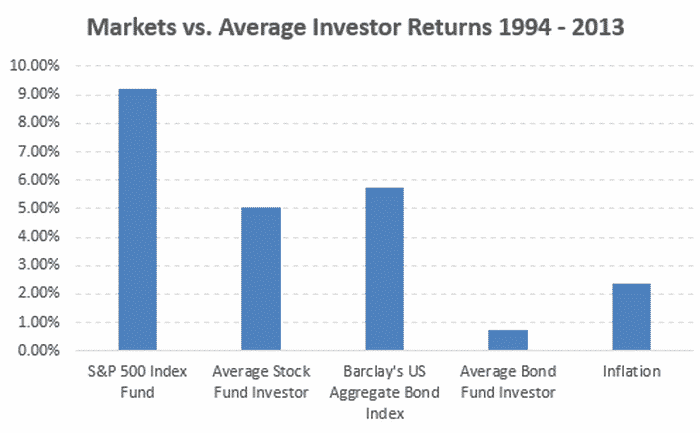

Term insurance is pure insurance. It isn’t connected to an investment. If you get 20 year term insurance, and you don’t die during this period, you won’t get anything back.

With whole of life insurance, it is connected to an investment. So even if you don’t die, you might make “a profit” from the insurance.

On first glance, whole of life seems the better deal. In general, however, term insurance is the better deal and getting investments separately.

This is because with term insurance, you are paying for the costs of the investment and insurance.

This typically means you get much less coverage on the insurance side, and sub-par investment returns, as the costs of the investment are high.

Zurich Futura Review

Zurich International is one of the biggest insurance firms in the world, and has offices in Qatar, the UAE and beyond.

It is no surprise then, that their insurance products are widely sold. Size doesn’t always equal better policies, however, and this is certainly the case with this policy.

It is more expensive than some of the other plans reviewed below, due to its whole of life nature.

So how do the plans work? In addition to the life coverage, one of the positives of the plans is that you can add many waivers.

Those include critical illness, family income, hospitalization, permanent disability and a few other options.

You also have flexibility in terms of which currency to pay the plans in, how often (say monthly or yearly) and you can adjust the premiums if your circumstances change.

You can also add or remove benefits and encash your policies if you no longer require it.

So what are the negatives? The main negatives are:

It is expensive as you are getting the cost of the insurance and investment.

The actual investments inside the Futura can be very expensive.

If you encash in the early years of the plan, even the first 7–10 years, you might not get much back. Considering you are getting less insurance in this plan, compared to cheaper term insurance, this is a tough pill to shallow.

If the investment returns are lower than those you expect and have been ‘promised’, you may need to increase your premium to keep the same insurance benefits.

If you make withdrawals, your policy can lapse.

There are no index tracker options within the Futura, so many of the mirror funds used are expensive.

There is a loyalty bonus after 10 years, but there are many terms and conditions associated with this being paid.

The charges are very high. Just to give you one example, all single premiums are charged at more than15% a year!

The old school processes makes doing anything difficult, including withdrawals and change of address.

Zurich International Term Insurance Review

Compared to the Futura, the Zurich International Term Insurance is cheaper and an overall better product.

As this is term insurance, you won’t get anything back, however, if you don’t die during the term.

The key features of the plan are:

Terms of between 5 and 35 years.

You can maintain protection worldwide. So even if you move, you can still maintain coverage.

Like on the Futura, you can add optional benefits like permanent and total disability.

The positives of this plan are:

The costs are much lower than the Futura. Not the lowest in the market, but much better.

The negatives are:

Zurich’s customer service isn’t always the best. You are merely a number to them. I have seen processes like withdrawals take months to complete due to something incredibly small — like your signature isn’t a 100% match with the original or you have moved address so need to complete a new form.

Zurich won’t pay claims if you haven’t been honest on the application form. That sounds reasonable. However, in addition to that, you can’t claim if you haven’t paid all the premiums due. There are also additional restrictions like terrorism.

Even if you wanted this plan, new policies aren’t sold in many countries anymore. You can only buy this policy in a few countries.

It is still more expensive than some of the other plans in the market.

Rl360 LifePlan Review

RL360 is an insurance and investment company based in the Isle of Man. Their LifePlan product is more akin to the Futura, in that it is a whole of life insurance which is linked to investment units.

The main features of this product are:

$200 a month minimum premium. You can pay in 4 currencies.

You can get covered up to $7.5M.

You can add waivers like critical illness. This benefit is capped at $750,000 per year.

You can also add total disability and other waivers.

You can also add business coverage (like key man insurance which protects your business if a key person in your business dies) and family protection.

The positives of this plan are:

It does offer a good range of benefits, combining business, family and personal needs. This would be great if these benefits were good value, but this isn’t the case with this policy. It might seem convenient to pay for business, personal and family coverage in one policy, but most of the people who buy this plan are eventually unsatisified.

The negatives are:

It is expensive. Almost as expensive as the Futura. Fund costs are usually 2%+ per year. There then are additional costs that can total another 2%-5% per year. Much cheaper options are available in the market.

You are dependent on the investment and insurance elements of the plan. This means you might have to pay more for the insurance, if your fees eat into investment performance.

It is too complex with too many restrictions.

Friends Provident International Protector Review

Friends Provident has offices in the Isle of Man, Hong Kong and Singapore and has decades of experience in the international expat investing and insurance scene.

The term insurance they offer is pretty solid. The options offered are:

Term life insurance.

Term life insurance + critical illness coverage.

Critical illness cover as a stand alone product.

Like most life plans, there are maximum ages for buying this insurance. That is, 65 for life cover, 55 for life total and total disability and 60 for critical illness.

The main positives of this plan are:

Much cheaper than most products in the market.

Benefits can be tailored to your needs. For example, you can choice level or decreasing term insurance. You can also pay in numerous currencies.

With level life insurance, if you die during the term, your family gets the same benefit level. With decreasing life coverage, that benefit gradually falls over the years. Decreasing life insurance is often used in conjunction with paying off a specific debt — for example a mortgage.

It is probably the cheapest of the 4 insurers I have reviewed here.

No additional and hidden charges (in most cases). For example, no credit card charges.

The main negatives are:

You can’t buy this policy in most countries these days. It is only available in a few countries, unlike before 2014.

Certain restrictions do apply such as if you die playing extreme sports, terrorism and war.

Even though it is cheaper than the other plans reviewed here, for many people there are cheaper or better options, depending on your circumstances.

Just like all of the other providers, bigger insurance providers and banks, live off their brand names. A lot of boutique insurers are just as safe, and can’t rely on their brand names, so need to offer better benefits.

What about if you already have any of these four plans?

If you already have these plans there are 3 options:

Keep paying in until the end.

Stop paying and withdraw the money from the policy (in the case of the whole of life insurance). With term insurance stopping payments means you have no surrender benefits.

Stop paying in but maintaining the money in the investments. In other words, you leave the investment component alone.

In general, if you are paying for term insurance already, it doesn’t make sense to switch to another provider, unless it is cheaper.

With whole of life insurance, it usually makes sense to withdraw money or stop payments, if you then buy cheaper term insurance.

For example, if you are paying $700 a month now with whole of life coverage, you might be able to get term coverage for $200 a month and invest the $500 into a low-cost investment.

The big mistake most people make is engaging in “loss aversion”. It is human nature to find losses at least twice as painful, as gains are pleasurable.

In other words, accepting a loss is painful, even if you can make up for the loss in just a few years.

So many people think “i don’t want to accept a loss considering I have already paid in 50k or 100k and can only get 20k back”.

Rationally and in terms of the maths, taking a hit can make sense medium to long-term.

Why do people buy the more expensive whole of life policies?

One of the main reasons is that people believe there is a “free lunch” where they can be insured, and get the benefits of an investment account. In reality, you pay for these things.

With term insurance, moreover, many people are worried about losing money if nothing happens.

However, insurance is merely a protection against statistically-speaking unlikely events.

Do expats need life, income and/or disability insurance?

Whether you need these insurances depends on many things. In particular it depends on:

How liquid your assets are. If you are dependent on illiquid assets that are hard to sell or take months/years to sell (houses and businesses), you should consider term insurance.

If you have kids, or plan to have them, or dependents, you should consider term insurance.

If your income is not protected, you should consider term insurance, especially if your family is dependent on your income.

In other words, if you are a government employee, that has been sent overseas, with full income protection, your situation is very different to a self-employed person with a volatile income.

Likewise, if you are married to somebody with a similar income to yourself, you are more protected, in many ways, than if the family has just one income to rely on.

What are the main negatives all 4 options have in common?

Two of these plans are much more expensive than the other two. All have the following negatives in common, however:

They are all “old school”. Physically application forms are often needed. It can take a month, yes a month, to have cover in place. In comparison, some other options can have coverage in place within 24–72 hours. Some of these providers are investing in technology, and trying to improve speeds, but they are still not quick.

Even after the coverage is set up, you often need to send forms by DHL, for small changes to the policy.

They are all relying, to varying degrees, on brand name. Newer or lessor known firms need to lead on product benefits and ease of processes to a greater degree.

For income protection, there can be many restrictions about who can apply.

What are the risks with life insurance?

The main risks with life cover is that:

Inflation erodes your payouts.

Currency falls affect your payouts. For example, you have gotten your coverage out in GBP, but the Pound has fallen recently.

The coverage will stop as soon as you stop your payments.

The investment performs badly (this is only a risk with the whole of life coverage).

The insurance firm goes out of business. This is a relatively small risk, though, and checks and balances exist for investment-linked life insurance such as limited government guarantees.

The amount of insurance you need will increase with age, but you can’t increase the limit, for numerous reasons, such as your age or general health.

Premiums will rise as you age. Some of the providers, like Friends Provident, guarantee the premiums for 5 years, depending on the cover you pick.

You don’t get covered in the first place as a medical exam is expected or for another reason.

How are pre-existing conditions usually defined?

It differs depending on the insurer. Some insurers define it as a condition in which you have received treatment for in the last 5 years, and others define it in a more liberal or strict manner.

How can you have than one beneficiary?

Most life insurers allow you to pick multiple beneficiaries.

What if the predicted cost of coverage increases?

Whilst some insurers such as Friends Provident offers the 5 year guarantees, that doesn’t prevent insurance policies rising in all situations.

If this happens to you, you typically have 2 options; increase your premiums to retain the same benefits or lower your benefits and continue to pay the same premium.

How about the banks and local insurance firms?

In general, the expat banks charge a lot for life insurance. When it comes to local coverage, it depends on where you live and your circumstances.

In most situations, it makes sense to get expat coverage. Local coverage can make sense if:

You live in a country which has good-quality insurance options and has the rule of law.

Usually if you are an expat in the USA, local coverage makes sense, for legal reasons.

If you live in developed country and your husband or wife comes from that person. For example, you are married to a Singaporean, Japanese or Australian person, and you are getting the coverage for them.

The last point is especially important if your partner doesn’t speak much English. This point can be negated with some of the more tech-savvy life insurance firms which makes claiming easy.

I heard many insurance firms don’t pay upon death?

Provided you haven’t lied on your application form and have heard the exclusions, the policy should pay as expected.

The bigger issue is value for money, rather than not paying.

Do you offer insurance?

My main services are financial and investment management services. I do offer insurance.

I tend to prefer the lower-cost, online-based (or heavily technologically-dependent firms) as they can offer expats and indeed locals better insurance options, for a cheaper price with less hassles.

Sometimes I can offer discounts on the stated online price as well.

What are the biggest mistakes expats make with life insurance?

The biggest mistakes I have seen in the expat market are:

Assuming that brand names matter, especially brand names linked to our home country. In particular, assuming that big insurance firms are likely to pay out claims more quickly. In fact, they are usually overly bureaucratic and slow.

Due to the last point, many expats end up buying expensive policies.

Getting whole of life insurance, at least in most situations.

Not getting enough coverage, or too much. Not working out how much is needed in a mathematical way. The people who are most likely to assume they don’t need coverage are business owners. The kinds of business owners that have a lot of on-paper wealth, but it is often held in illiquid assets.

Knowing you need coverage, but delaying, and eventually paying more. Often times, you get better premiums when you are younger.

Thinking the life insurance firms needs to have an office where you live. It is best to focus on a firm that has online processes which allows you to claim no matter where you are in the world.

Thinking that it is a good idea to have life, health and income protection from the same insurer. This only makes sense if each product is good.

Conclusion

Most expats do not need whole of life policies, which are more expensive. Term insurance is cheaper, together with doing investments separately.

From the four policies reviewed here, two are much cheaper. However, these two options are more difficult to buy these days and/or cheaper options exist in the market.

The amount of life coverage you will need as an expat, will depend on several things, including your lifestyle and liquidity of assets.

In general, expat coverage makes sense. In certain, limited situations, getting local coverage can be worthwhile.

Further reading

For expats who have existing investment policies held offshore, the article below would be useful reading.

It includes countless comments at the bottom from people who hold the policies.

(please note this article originally appeared on adamfayed.com)

Updated September 21, 2019

As some of my more frequent readers know, I have spent more time in Japan and China, than any other country apart from the UK.

After 8 years living overseas, what are the key mistakes I see expats make when it comes to financial planning, investing and business?

The information below are the most common mistakes I have seen in the expat community in Japan, and how you can mitigate them, alongside answering some FAQs.

Those FAQs include Japanese inheritance tax issues, which concern countless expats living in Japan, and deductions.

This article is long and covers many issues. For those that are time-poor and want financial advice, please email me on adamfayed@hotmail.co.uk or adamfayed@int-amg.com

1. Keeping up with the Jones’

Japan isn’t as obsessed with consumption as Singapore, Hong Kong or Dubai. Despite having more millionaires than any other city on some metrics (although not on a per capita basis), Japanese people aren’t flashy as a generalization.

That doesn’t mean a minority aren’t, or your fellow expats aren’t. Many expats are on big packages, but remember that Tokyo is an expensive city, if you factor in the tax and rents.

$200,000-$500,000 a year might sound like a lot of money to most people, but once you adjust for the taxes, cost of accommodation and sometimes international schooling, it can go quickly if you put your mind to it.

I have seen expats on 250,000-350,000 yen a month ($2,300-$3,300 or so) gradually increase their wealth, and others on $500,000 a year, who are in debt or have zero wealth!

Remember wealth is net income – expenditure x compounded returns. If you spend more than you make, to impress people you don’t even like, you will get into trouble.

So your spending and investment habits make a bigger difference to wealth than your income.

Just ask Mike Tyson, Boris Becker or Michael Jackson- having a super-high salary isn’t an automatic passport to riches!

So use your expat package wisely!

2. Not reviewing inheritance and estate planning

The Japanese Government can potentially tax you significantly if you die. So planning is key if you are going to be a long-term Japanese expat.

This is especially the case considering these rules are always changing.

3. Focusing on local real estate

Real estate doesn’t outperform markets long-term, in most cities and situations. The biggest advantages of real estate are leverage and rental yields, but that has become harder to profit from in Japan.

There used to be a time when capital values were stagnant, but using Airbnb was a simple way to get good rental yields in Tokyo and beyond.

That has gotten harder with new government rules and restrictions. In general, unless you are a professional real estate investor, it is best to use real estate as a home or just rent.

If you are in Japan on a short-term contract, renting makes sense. If you plan to stay for 20-30 years, then buying on a mortgage can be cheaper.

4. Not reviewing your existing investments

Most expats in Japan have expat investments held offshore. Some people are getting good returns, and some are not.

Markets have performed well for 10 years or longer, so your portfolio should be performing well as well.

You should also review your pension situation in your home country, to see if you can limit tax.

For British people, and some other nationalities, there can be significant tax benefits to transferring a pension overseas. This is especially the case for larger pension pots.

At the bottom of this article, I review some of the most popularly sold expat products in the expat community.

Many people make the mistake of never reviewing these policies.

5. Focusing on local solutions for your investments

As somebody who has lived in Japan, I can say that it makes no difference where your advisors lives, in this day and age.

What matters is things like fees, how long you invest for, what you are invested in and how easily you can communicate with your advisor.

Some expats tend to localize too much and get used to overly conservative business norms, like focusing on face-to-face communication.

They meet an advisor at an event, or get recommended to use X and Y company, and don’t consider the alternatives such as an online advisor.

Ultimately an online advisor can do things more quickly, efficiently and cheaply compared to somebody with a big flash $30,000 a month office in Roppongi.

That money comes from clients money. If they are wasting time with endless chit chat, which tends to come hand-in-hand with face-to-face meetings, I doubt they can respond as quickly to your emails and inquiries as somebody who is using the latest technology remotely.

I should know. I used to do things the old-fashioned way and know how inefficient it is compared to the alternative where clients can flick me a message on WhatsApp and I can reply within hours at most.

It also needs to be remembered that local solutions are often more heavily taxes.

6. Giving money to a partner

Speaking about localization, unless your wife (or indeed husband) is financially qualified, there is no reason for them to look after the money.

It makes sense for decisions to be jointly made, or for the wage earner to make those decisions with the help of an advisor.

Giving money to a partner seldom works out well, and causes untold complications if you get divorced.

Many expats, especially men, tend to justify this norm as being a Japanese traditional. It may be a tradition to give money to your wife….that doesn’t make it rational.

7. Leaving money in the bank

The bank pays people 0% interest in Japan. This is lower than inflation and even lower than the US and some other countries.

Most developed countries now have negative real interest rates according to the Economist Magazine’s stats below;

So you are guaranteed to lose money with this tactic. Investing, as opposed to saving money, makes the most sense.

Don’t get me wrong, markets go up and down. However, the long-term has always been good.

As Buffett pointed out 1-2 years ago, $10,000 invested in the S&P in 1941, would be worth around $52m today!

For that matter, $10,000 invested in the early 1990s, would be worth $100,000 today. There is no reason to be afraid of short-term fluctuations in the market, especially if you have government bonds in your portfolio.

8. For business owners – not focusing beyond Japan

As mentioned before, your wealth is net income – expenditure x compounded returns. For business owners, you have a great chance to increase your wealth, compared to a salaried employee.

It isn’t easy in a stagnant market, however, so many Japan-based business-owners need to be enterprising. Many fail in this regard and become insular.

In Singapore and various places in SE Asia, it is normal for people to use their locations as a hub. Business owners, who just live in location A, but target location B or indeed the world, from their laptops.

In Japan, 95%+ of expats seem to be either salaried employees, businesses focused on Japan or those focused on things like inbound tourism – Chinese and other foreign tourists who are coming to Japan on holiday.

What I seldom see in Japan is enterprising people who use Japan as a base for global business.

I have met a few. I met one man who only came to Japan due to his wife being a local. He uses Japan merely as a home – a nice and comfortable place to live.

He works from work, on his laptop, and doesn’t target the local market any more than any other market. Only 2% of his revenue comes from the local market.

Likewise, for me, my location is irrelevant. That isn’t just words, I have gained clients in 27 countries (and 5 continents) in the last 12 months alone, and I haven’t focused on local markets since 2014.

Not since 2014 have I gained the majority of my clients in the country where I was resident. The fact is, we live in completely different times now with the digital age.

This isn’t just affecting business. Even 5-10 years ago, people would have found it incredible, to think that a man relying on Twitter, and being outspent by his political rival 2:1-3:1, could beat his political opponent in the Presidential Elections of 2016!

And then barely a few months ago, an enterprising 28-year-old Democrat, Alexandria Ocasio-Cortez, beat the 4th highest ranking Democrat by using online tools.

That could never have happened in the 1950s, 1980s, 1990s or even 10 years ago when this digital revolution was just getting started.

The digital age is affecting business as much as politics. The business practices from the last 200-300 years are changing. We are in the middle of different age, a digital revolution.

The internet has been around for decades, but only in the last 5-10 years, are we doing more and more things online.

What is the first thing you do now? You Google probably, just as I do! And unlike 15 years ago when we only trusted Amazon and eBay and big companies, these days people rely on online recommendations and the authenticity of a personal brand/relationship.

When I am the buyer, the LAST thing I want to do, is takethe subway and meet you face-to-face. I want credibility through online recommendations.

I want speed and accuracy. 20 online recommendations on LinkedIn matter 10x more to me than how you are dressed, or which office you work from.

Many people feel the same. And yet, perhaps due to Japan’s old-school culture, many long-term expats in Japan still focus on business cards, face-to-face communication, outdated rituals and only focusing on the local market.

I remember I had a chat with a country manager of a major MNC in Japan a few years ago. He told me he doesn’t like to hire expats who have lived in Japan for more than 5 years, or especially 7 years.

The reason? They become less enterprising. More conservative and localized. Try to avoid this trap.

So If you have a business in Japan, focus on the world from your fingertips, not one market with stagnant growth!

Of course, not all businesses can be scaled online. Many can though.

9. Underestimating certain things

Underestimating the cost of living, how much you need to save for retirement and how many years you will live in retirement, are mistakes made by expats in Japan and beyond.

It is easy to get into the habit of wishful thinking, but just remember we are also in changing times when it comes to medical technology.

You may easily have 45 years+ in retirement!

10. Getting stuck in a rut

Especially if you own your own business, executing ideas can be key. Ideas in isolation are irrelevant. Execution matters.

Effective execution becomes harder when you associate with negative and toxic people or get into regular habits.

I found moving from country to country every 2-3 years, and regularly speaking to people in different industries online, can help keep my brain fresh.

Of course, this option isn’t available to everybody, but I have found some expats come to Japan full of energy and vigour, and soon become negative after 3-7 years.

That negativity can indirectly affect sales, business and even spending habits – a lot of the aforementioned bad spending habits is caused by boredom.

11. Putting all your eggs in one basket – especially illiquid assets

Too many expats in Japan, or indeed globally, just invest in their business. Or just in property locally or back home. Or just in stocks.

Realistically, you can’t rely on an illiquid asset in retirement. If you get sick tomorrow, could you sell your house or business?

Especially if your business is highly related to your personal brand, contacts and skills, why would somebody want to buy that business, if you aren’t going to be around?

I have met countless people who have boasted to me about land, property or business valuations but have failed to sell those assets when they most need to.

It makes sense to have assets in relatively liquid stock and bond market portfolios, to limit the risks, whilst still gaining from rising markets long-term.

That doesn’t mean you shouldn’t invest in your business. Reinvesting money into your business can have a great return on investment, especially when your business is small and growing fast.

But again, we are in changing times. So cheap and free techniques can be more effective in 2019, than expensive options.

I know countless people today making more money from cheap Facebook ads than they do from $10,000 promotions.

I also know many people who are able to make more money from writing articles, than they do going to events.

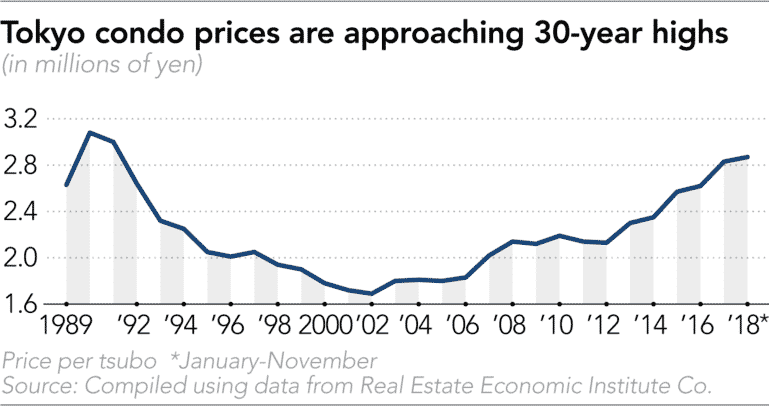

Finally, let’s not forget that illiquid investments like property are amongst the most expensive in the world in Japan.

They are now fast approaching the levels last seen during the Bubble Economy:

12. Comparing yourself to people back home

You probably know people who are earning $40,000 or 40,000GBP in retirement.

I am from the UK, and I personally know countless people who have the Old Age Pension + rental income + a company pension in retirement.

Most people consider such people merely comfortable at best, and certainly not rich.

And yet, $40,000 is the equivalent to $1m benefit, if you were to invest for yourself.

The reason is simple. If you are drawing down a retirement pot, it is only safe to withdraw 4% of a portfolio.

Why do I mention this? Well, many expats console themselves that “I am saving and investing more than my friends back at home”.

That might be true, but remember, they have additional social security benefits.

That isn’t to mention other benefits like healthcare. Many expats have higher cost of living in retirement, due to not paying into the healthcare system.

So investing for expats is more of a necessity, rather than an added bonus. So don’t delude yourself that saving just a bit more than your peers back home, is enough.

Frequently asked questions (FAQS)

This section will answer some FAQs I am asked by expats – especially those which weren’t addressed above:

Should you invest in Japanese Yen?

Unless you are actually going to retire in Japan, saving and investing in Yen doesn’t always make sense.

The Japanese Stock Market is, on many measures, riskier than US markets and something more diversified like MSCI World.

If you don’t know where you want to retire, focusing on USD- based investments can make sense.

If I invest overseas, whilst living in Japan, what if I leave?

Most of the investments that can be utilized are portable and thus can be transferred.

Do most DIY platforms accept for Japan?

Some do, and some don’t, and the rules are always changing. It is always best to check with the platforms you are interested in setting up.

Otherwise, ask your advisor for help

Do you have clients in Japan?

Of course.

What about inheritance tax in Japan?

Inheritance taxes can be high in Japan – up to 55% in fact! So if you die whilst living in Japan, this can hit you hard.

The rules are currently being reviewed, but you shouldn’t rely on changing rules.

You should always “plan for the worst, but hope for the best”. A good advisor can help you set up quality options for estate planning and inheritance tax reductions.

How to calculate inheritance tax, is complicated, as it depends on several factors including what visa you are on, how many years you have lived in Japan and the location of your assets.

What is Judsho?

It is understood to be the place where you are resident for tax purposes. Before 2013, if a person’s “judsho” was outside of Japan, they were only liable for inheritance tax on assets held inside Japan.

That has changed, which means that there is a “worldwide inheritance tax” system in Japan.

Those laws were changed in 2017, to ensure that only those that have lived in Japan for more than 10 years would be hit by this worldwide inheritance tax rate.

In 2018, that was further changed to 5 years, as a trail.

What are the inheritance tax rates in Japan?

The rates are:

• Up to ¥10 million ………………… 10%

• ¥10 million – ¥30 million ……… 15%

• ¥30 million – ¥50 million ……… 20%

• ¥50 million – ¥100 million ……. 30%

• ¥100 million – ¥200 million ….. 40%

• ¥200 million – ¥300 million ….. 45%

• ¥300 million – ¥600 million ….. 50%

• Over ¥600 million ……………….. 55%

Are there many exemptions from inheritance tax?

The following exemptions apply:

¥5 million retirement allowance per each heir

¥5 million life insurance proceeds per each heir

Various non profit exemptions

Foreign tax credits

There are other possible exemptions as well, including if the heir has disabilities.

Real estate and local businesses also have deductions.

When do people need to pay these taxes?

You need to pay these taxes within 10 months of the death.

What things are never likely to change?

Japanese-sourced assets are always likely to be taxed. As Japan tries to attract more foreign talent, due to the falling population, foreign investments may continue to be liberalized.

Contact details

adamfayed@hotmail.co.uk is my email and I am online on a range of apps. My services range from monthly and lump sum investments, through to reviewing existing investment portfolios to see if I can offer greater growth.

A range of client recommendations can be found online

Further reading

For expats in Japan, or globally, that have existing investments, the following article would be useful.

It reviews some of the most widely sold plans in Japan, and globally. Countless expats have these high-fee and underperforming investment plans, which they have left dormant.

(Please note this article originally appeared on adamfayed.com)

Updated September 21, 2019

Salary packages in Dubai, Qatar and other Middle Eastern countries can be high, for certain industries at least.

The region is also a hub for entrepreneurs. Tax-Free living should theoretically make saving and investing vast sums of money easy.

However, I have met countless expats in the region who aren’t meeting their financial goals.

In fact, about 25% of the people who reach out to me online, are living in the region. This article will consider why that is and give some general financial tips.

This article will review the biggest mistakes expats typically make, alongside answering some frequently asked questions.

This article is long. So for the time poor expats who are looking to invest or get a second opinion on an existing investment, please email me — adamfayed@hotmail.co.uk.

What are the biggest mistakes expats make in Dubai and Qatar?

Speaking to expats in the region, who often approach me after getting previously bad advice, or getting into bad habits, the following things are the most common mistakes;

1. Wanting a local advisor.

Whilst this is changing, as more and more things go online with financial services being no exception, some expats still want a local provider.

This means having a flash office in the centre of Dubai. With a lot of admin support and other things. Ultimately, however, who pays for those facilities?

The client pays. An online provider can usually do things more cheaply, efficiently and quickly than somebody who is using old school methods.

It is also safer in many ways. An online broker is much less likely to go out of business, compared to a firm with huge overhead.

I have met countless firms who have gotten into cash flow issues, and the main reason is their $30,000-$50,000 per month office costs.

Let’s not forget as well, that you will probably leave Dubai or Qatar in the future. Many expats move every 3–4 years, and want an advisor to follow them, whenever they are located.

So having an advisor who utilizes technology can be key. Flicking your advisor a message on WhatsApp or email, wherever you are in the world, is much more convenient than old school ways of doing business for the time-poor.

In addition, many investors get attached to financial advisors from specific countries, such as their country of origin.

For example, many British people in Dubai have UK advisors, whilst the majority of Indian expats have employed Indian financial advisors in the region.

In certain instances this can make sense. Sometimes in very specific cases, such as tax-related cases, such advisors may have specialist knowledge or qualifications.

When it comes to most types investing though, the key things are investment returns, fees and communication.

This isn’t nationality-specific. My non-British clients, to the best of my knowledge, are no less happy than the Brits!

2. Not cashing out bad policies

Nobody likes losing money or even declining markets. Sometimes, moreover, a decline is temporary. Look at 2008–2009. The markets crashed and came back strongly.

In other situations through the fundamentals of the investment are bad. This is especially the case with costly and opaque investment vehicles. Often times, cashing out and taking the hit, makes sense.

I will give you a simple example. Let’s say an expat invested in a $100,000 policy in 2012. The value eventually falls to $90,000 in 2013–2014, despite rising markets.

The person eventually sells the investment in 2017, for $103,000. At least they didn’t lose money, right? However, in that period, US Stock Markets increased by more than 10% per year on average.

Selling out at $90,000 would have been painful, but many lower-cost investments would have made up the $10,000 loss, from taking the $90,000 in 2012, within 13–14 months.

3. Keeping up with the Jones’

Dubai and even Qatar to an extent have a materialistic culture. I was struck by how many people seemed to be showing off, the first time I visited Dubai in 2007.

Many expats get into the habit of spending money they don’t have, to buy things they don’t need and/or want, to impress people they don’t like or respect.

I have seen many expats on huge packages, who don’t save or invest $1, or even get into debt!

4. Home country bias

It is human nature to be more reassured by the familiar. Psychologists call this familiarity bias. Sometimes, though, it is a huge mistake. This is especially the case with investing.

I am from the UK, as most of my readers know. However, does it makes sense for me, as an expat of 8 years and counting, to keep most of my wealth in Pounds?

And to keep my investments purely in the UK FTSE100, UK property and UK Sterling? Clearly not, especially with Brexit and the Tory Leadership contest going on, as we speak.

Familiarity bias also causes people to invest in local stock markets, as they become more familiar with the names listed on the exchanges.

In the case of Dubai or Qatar, there aren’t many good reasons to invest in the local markets, as opposed to the S&P50, MSCI World or numerous other indexes.

5. Speculation

Trying to market time, stock pick and buy and sell coins, are all forms of financial speculation. Being a speculator and a long-term investor isn’t the same thing.

It is also a mistake to assume that only kids and irresponsible people invest in such schemes.

Investing in high-risk schemes like FX isn’t a scam in most cases, but is ultra high-risk. Ultimately, people from all backgrounds can get into the extremes of greed or fear.

6. Not considering your tax situation

Regardless of your nationality, it is important to remain tax-compliant. If you are American, you need to consider your tax situation when you invest overseas.

If you are British, you shouldn’t need to pay tax on your overseas income, assuming a few conditions are met.

You do need to pay tax on your UK sourced income, though, including any capital gains from property or markets.

Considering local taxes is also important, although the tax system in Qatar and Dubai is fairly simple and straightforward.

7. Thinking brand names matter

Most people like to feel safe. That is human nature, but assuming that big brands are safer can be a big mistake.

I spoke to an expat in Dubai 3–4 weeks ago. He is getting very poor investment returns, despite markets performing very well in the last 10 years.

When I asked him why he picked the specific product, he said that the firm sounded like a huge name.

I won’t mention the name of the firm here, but it is one of the biggest insurance companies in the world, that offers insurance-linked investments.

Big brands can get away with charging more because they will still get clients regardless of their charging structure.

Often times boutique and specialist providers can offer better services, at offer costs. This doesn’t just apply to finance, either.

I have certainly had better experiences with boutique hotels, recruitment firms and medical clinics than big brands and I guess you have too!

8. Not considering your UK pension situation carefully

Many UK expats transfer their pension schemes overseas. Whilst there are many good reasons for this, including tax benefits, there are positives and negatives involved in transferring a pension.

For smaller pension pots, the fees for transferring the pension offshore can eat into the gains of taking action.

The investments that you are in, moreover, should also be considered. There is no point in transferring a pension offshore if your investment returns will be poor, regardless of the tax benefits.

9. Focusing on local property

We have already spoken about familiarity bias and how it can affect investors. Property is another example of this.

Dubai and Qatar are not cheap property markets. That doesn’t mean that you should never consider buying a property.

There will be plenty of people, especially professional real estate investors, who make a lot from property in the region.

If you plan to live in the region for 20–30 years, you may also just be using property as a home rather than an investment.

However, assuming renting is always dead money, is a key mistake. Renting can be cheaper than buying as many academic studies have shown.

It is less time consuming as well. If your boiler breaks tomorrow, your landlord or the property management company will have to fix ir, and pay to alleviate the issue.

As time is money, and many expats are time poor, renting can make a lot of sense.

10. Insurance

Insurance is a necessary evil for most expats living in Qatar or Dubai. However it is a dead-money product.

It isn’t like an investment, where you are rewarded by investing more. Therefore, you should spend as little as possible, for getting as much as possible.

I have met several expats overpaying for insurance. Getting a cheaper option on renewal makes sense.

When it comes to life insurance, you don’t need it, unless you have kids or plan to have them. If you do have kids or a dependent, cheap term insurance is much better than the more expensive insurance-linked schemes.

Insurance and investing should be kept separate, as a generalization.

11. Leaving the money in the bank

At the opposite end of the extreme to greed, fear can consume many potential investors, who are petrified by market volatility.

It is understandable because finance and investing can seem confusing for most people. This isn’t helped by the media, who engage in sensationalism whenever markets fall.

However, leaving money in the bank, whether in Qatar, UAE or the UK, is a losing long-term strategy.

These days the banks pay close to 0%, and even if you lock away your money, beating inflation isn’t easy.

You can’t realistically, therefore, save your way to retirement, especially when you are living overseas, outside your home countries social security system.

So investing, as opposed to saving money, is important. Long-term investing isn’t dangerous, even though markets are volatile.

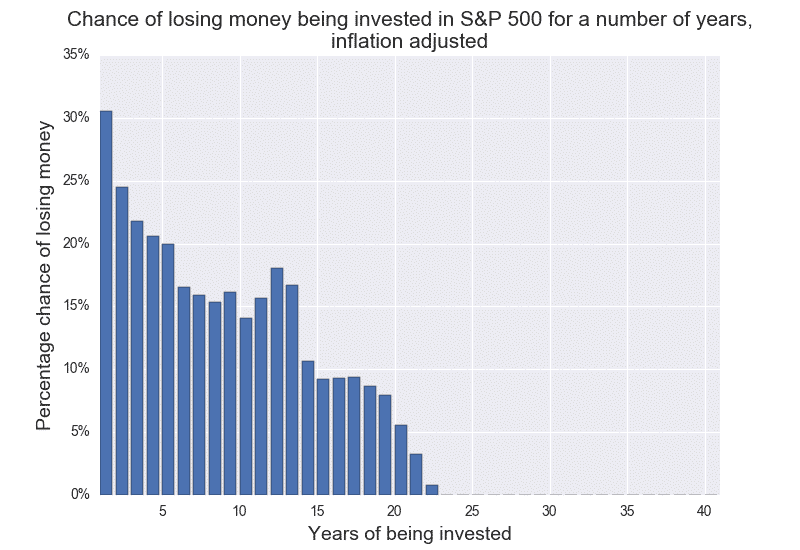

The Dow Jones was trading at 66 in 1900 and hit 26,800 this year. $10,000 invested in the S&P in 1942, would be worth $50M in 2019, but there have been many bad times for markets.

Historically, you have a 28% of being down over a 1 year period, and a 72% chance of being up.

That falls to a 10% chance of being down over a 10 year period and 0% over 20–25 years. In other words, a buy and hold investor, who doesn’t panic, has never lost in markets.

I am not implying that just because something has never happened before in the 200 years of markets being around, that it can’t happen in the future.

However, having your money in a combination of 3–4 major stock markets and the bond markets is a long-term winning strategy.

Markets are just the biggest firms in the world, after all. They do tend to get more profitable and efficient over time, due to technology.

12. Not factoring in purchasing parity

Dubai and Qatar aren’t cheap places, despite the lower taxes. It might sound obvious, but you need to consider the local cost of living.

I have met countless expats who have considered offers at the end of their 3–4 year contract.

Many do not consider the various cost of living implications and reject opportunities on this basis.

I have one British client who didn’t want to earn $5,000 less per month, for relocating to Vietnam.

When we went through the figures, however, his ability to save and invest had probably increased, due to the lower costs of living.

13. Focusing on illiquid assets

Many successful business people have growing businesses. They assume they don’t need to invest, due to having a valuation like $3m.

The same with many property owners. However, consider that it isn’t always easy to find a buyer for an illiquid investment.

It can take months or years to find buyers, especially for businesses. In the meantime, if something unexpected happens to your health, you may be left with little income.

I have lost count of the number of struggling business owners that were affected by the Saudi blockage of Qatar.

I have also seen several business owners go out of business in the last 10 years, in places such as Thailand, Tunisia and Egypt.

The point is, too few people “hope for the best but plan for the worst”.

14. Comparing yourself to people back home.

People in your home country might be paying into the social security system. This can be a huge benefit.

As an example, the UK’s Old Age Pension might sound like a tiny benefit, but $10,000 a year is the equivalent of having $250,000 extra in retirement if you were saving for that benefit yourself.

This is because the “4% rule of retirement” dictates that you can only safely withdraw 4% of a retirement pot every year.

The point is, there are many people in the UK, Canada and beyond, that don’t save and invest anything.

However, they are often paying into government and company pensions, which means they might have 40,000 or more in retirement, without investing additional money.

$40,000 is the equivalent of saving and investing $1m on your own, given the aforementioned 4% rule.

Yet I have seen many expats claim “I am saving and investing more than people back at home”, forgetting that those people often have access to additional benefits.

So as somebody who doesn’t have access to these benefits, you need to try harder to invest and make up for this deficit.

That isn’t to mention that your cost base in retirement might be much higher than many of your friends back home.

Do most people need financial advisors whilst living overseas?

I have met countless expats who have read a lot of financial books. Some are time-rich as well.

Expat retirees would be one example or those who are semi-retired. Semi-retired consultants in the Middle East are another example.

On average, however, most expats are time poor and don’t feel they are experts in the area. For those expats, financial advice is often useful.

Beyond investment advice, general financial planning advice can be needed. Budgeting and financial plans seem simple, but simple and easy aren’t always the same thing.

Simple tips like using cash more, and your credit card less, and writing down a budget unique to every month, can make a huge difference to your budget.

As an example, studies have shown that people who use cash more, spend 2%-5% less, without even trying.

This is probably due to the fact that spending the money feels more painful when you need to give away something physical.

Often times getting this third-party advice can be useful.

What are the costs of investment advice in the region and beyond?

Different advisors charge contrasting fees. I charge 1% on smaller portfolios and 0.5% above $500,000.

As a generalization, the bigger firms (like life insurance companies and banks) charge much more.

How about robo advisors?

There are numerous robo advisors in the region, and beyond, that are available to UAE and Qatari expats.

Sarwa is one such example. Robo advisors can be very good, when it comes to basic financial advice, especially when used in tandem with an advisor.

They are not as good, when it comes to more complex issues, like estate planning, budgeting and so on.

I have written another article on robo-advisors, which is more in-depth, and can be accessed here.

How about financial advice in Saudi Arabia, Oman and other Middle Eastern countries?

The fundamentals of sound financial advice are the same all over the world, for expats and locals alike.

The main differences are your unique situation, and also some platforms don’t accept for certain geographical locations.

What are your contact details?

adamfayed@hotmail.co.uk and a range of apps.

Further reading

For expats with existing policies, including UK pensions, this article would be useful to read;

Many investors, and expats more generally, are confused by domicile and residency.

This might seem like such a boring topic, but it can affect capital gains and inheritance taxes.

This article will explain the differences between residency and domicile and answer some frequently asked questions (FAQs).

The article will also discuss new issues for “digital nomads” and tackle how you can invest in a tax-advantageous manner as an expat.

Is domicile important?

It is. It can determine taxes from your income tax to inheritance and capital gains taxes.

It can also affect inheritance tax planning.

What does domicile mean?

The country you are domiciled in is the place where you have your permanent home, or have a big connection with.

When you are born, you are usually assigned to your parent’s domicile. If your parents were not married, you are typically given the same domicile as your mother, although this depends on each situation.

Even when you move abroad, your domicile doesn’t usually change, unless you take specific action to change it.

What is deemed domicile?

For British expats who emigrate, there is such a thing as a deemed domicile. This can impact your inheritance taxes when you die.

Deemed domicile means that even if you are not domiciled in the UK according to HMRC law, you can be treated as domiciled in the UK at the time of transfer in two situations.

Namely, you were domiciled in the UK within 3 years immediately before the transfer or you were tax resident in the UK in at least 17 of the last 20 tax years, before making the transfer.

How about non-doms in the UK?

There are about 4-5m non-UK domiciles living in the UK, which can bring tax benefits.

However, in recent times, the UK Government has made significant changes to non-com status, after a populist backlash.

The number of wealthy UK residents who pay no UK tax on their offshore earnings has hit record lows.

There are many reasons for this, including political worries around Brexit, and the relatively new “non-dom” levy.

This is charged at 30,000-60,000GBP a year, in return for no tax on overseas income.

What is residency?

Your tax residency is the country you are supposed to pay tax to. It is a misconnection that if you spend less than 183 days a tax year, you are automatically considered tax non-resident.

Many tax authorities, like HRMC in the UK, have residency tests like the one below, available online;

It is always important to remember that rules about residency, including what defines ties, can always change.

So how would you summarize residency vs domicile?

Domicile means a legal residency where a person intends to make it their permanent home.

Residency is a more temporary thing in many cases. People can move with their expat job every 2-3 years, and change their residency in the process, without changing their domicile.

What is the difference between ordinary and multiple residencies?

To be an “ordinary resident”, the country has to be your ordinary home. You spend the majority of your time here and don’t take long trips home.

As an example, let’s say you are a British person living in the UK, but you take 2 holidays per year. You are an ordinary resident of the UK.

It is possible to be resident in two countries or more, although it can lead to tax issues.

Can people legally reduce their taxes by changing their residency?

Yes. If you get a job offer in Saudi Arabia, Kuwait or a country with 0% income tax, you are of course not taxed on your income unless you are American.

Americans are taxed on overseas income, even if they haven’t lived in the US for years.

There are also contactless countries that only tax locally sourced income. Singapore, Hong Kong, Malaysia and around 40 other countries fall into this category.

How about for digital nomads?

Many young nomads have this ideal life, where they are working on the beach from their laptop, moving from country to country.

Indeed, that is possible, and becoming easier, but that doesn’t mean you don’t have to be careful with your tax residency.

It is a misconception that you can just move from country to country, never spending more than 90 days a year in that place, and that means you automatically pay 0% tax worldwide.

Many people think that the “183-day rule” is simple. In fact, due to the rise of digital workers, many courts are asking expats to prove their residency.

There was a ruling in Australia, where an expat had to pay more tax, as he couldn’t prove where he paid his taxes, as he didn’t have a tax identification number (TIN) due the frequency of his movements.

Going forward, it will be safer for nomads to have at least one tax base, so you can answer the question “where do you pay your taxes” if it comes up.

I have personally seen a few nomads I know, have 2-3 years of “tax-free income”, only to be stung by an unexpected tax bill.

Can you buy a residency if you are a digital nomad or entrepreneur?

Countless countries do have residency programs, where you can get residency in return for making real estate and other investments, as outlined in the article at the bottom.

Some of these programs also offer citizenship, as well as residency.

Can this affect bank accounts and investments?

Yes, it can. Almost all financial institutions now, ask for TINs when opening up banks and brokerage accounts, although some will accept your old TIN if you have just moved to a new country.

What tends to be the most tax-advantageous investments for expats and nomads then?

For Americans, it can depend on several factors, as outlined in more detail here.

For British and many other expats, tax-efficient portfolio bonds have numerous tax benefits.

How can you lower your risks of unexpected tax bills?

In general, having expat banking and investments lowers your risks of tax bills.

The reason is simple. If you are from country A and live in country B, but keep your investments in country C, there are clear demarcations there.

In other words, if you are a British person living in Thailand, but your investments are held in Singapore or British Overseas Territory, you are keeping fewer ties to back home compared to if you send back substantial amounts of money every month.

In comparison, if you send money home to the UK every month, have 3 properties and 2 investment accounts held in onshore UK and so on, you are keeping a lot of ties to your home country.

Are changes likely in the future?

The last 5 years have been a period of change, with FATCA, CRS and various new laws coming into play.

There is no reason to believe the next 10 years will be any different, which is why it is important to work with somebody who is on top of changes.

Countless investors are interested in real estate, without the extra hassle of finding tenants, paying taxes and maintaining the place.

Others want access to real estate, but don’t have $200,000+ to invest. What can these investors do?

This article will discuss some options and answers some frequently asked questions, and also look at options for expats who want to invest in direct property but are struggling to get a mortgage.

What are the main options besides direct property?

This article will discuss three of the main options for gaining exposure to property without extra hassles; REITS, property funds and loan notes.

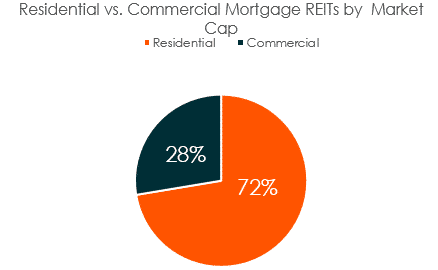

What are real estate investment trusts (REITS)?

REITS are real estate companies that invest in income producing property such as hospitals.

The average performance of some REITS has been impressive.An $100,000 investment in a Vanguard REIT index in 1996, would have grown to over $740,000 by the end of 2015, producing a 10.8% annual return, assuming dividends were reinvested.

This is slightly higher than the S&P. REITS come with some of the benefits of physical real estate, without the hassle of finding tenants and the other high costs.

REITS can be both commercial and residential focused, although residential dominates the market.

How to invest in commercial real estate through REITS?

Some REITS, like the aforementioned Vanguard REITS Index, tries to capture the whole market, like an index fund.

Other REITS are focused on specific segments, like commercial real estate, or countries like the UK, Australia or any number of other sectors.

Typically commercial and residential REITS are available on the same investment platforms as index funds and other forms of investments.

So is the easiest way to invest in REITS within an online investment account?

Yes, in general, the easiest way to invest in REITS is to open up an online brokerage account, which allows you to invest in stocks, bonds and REITS within the same portfolio.

This has the added benefit of allowing you to “rebalance” when one is doing better than the other.

What are property loan notes?

Property Loan Notes are financial instruments that are typically used to raise development capital for developers.

These loan notes have been particularly popular with regards to UK property in recent times.

They allow individual investors to invest, sometimes alongside institutional investors, in a development.

These developments can be commercial, or residential property. Like REITS, loan notes can sometimes be held within a wider stock and bond portfolio.

What are property funds and property index funds/tracker funds?

There are different types of property fund. One kind is fairly simple; some funds merely buy many construction and property companies or even merely just try to track the performance of a property index.

An example of this, would be some funds buy the shares of the top 100-200 property firms in the world.

Two examples would be the iShares Global Property Securities Equity Index Fund and the Vanguard Australian property Securities Index Fund.

Some property funds, in comparison, make more direct investments into the real estate.

Are these kinds of investments usually liquid?

Property index funds are almost always liquid, and you can take the money when you want. Most REITS are also liquid.

In the case of property loan notes, they often have a certain commitment period 2-3 years is a typical commitment period.

What are the risks?

All kinds of property have certain risks; political, social and otherwise. One of the bigger risks is the liquidity issue.

If a fund has too many people redeeming their investment, and too few new investors, they can get suspended.

This has happened with some huge funds, such as The M&G UK Property Income Fund , one of the largest of its kind.

This isn’t a big risk with a property index fund.

How can you invest in real estate for small amounts like 10k?

The easiest ways to gain exposure to real estate for small amounts of money, like 10k, is to have a 10%-15% allocation to something like REITS, within a broader portfolio.

The reason why this is effective, is many direct investments into REITS or property loan notes, have investment minimums.

In comparison, if you already have 100k-200k in an existing portfolio, it is fairly easy to start small with property investments.

Why don’t you personally invest much into direct real estate?

Many of my readers have asked me why I don’t own property, or at least direct property.

I do have a 10% allocation to REITS in my portfolio, and of course, index funds indirectly gives me access to property and construction related stocks without trying to pick winners.

However, the biggest reasons why I personally don’t invest in (direct) real estate directly is:

The time costs – real estate is less of an investment, and more like running your own business. You can’t rely on capital values most of the time, so need to focus on yield and leverage. So you have revenues from rent, and sometimes from the capital values once you sell, but you also have costs for taxes, maintenance and so on. You also have the time costs of being a landlord, especially if you go down the Airbnb route, which means checking in many tenants.

It isn’t easy to beat markets long-term – beating markets short-term, can and does happen, but over 40-50 years, it isn’t easy. What has made this situation harder, is that it is getting harder and harder to get 95%-100% mortgages, so leverage is getting harder in most markets. Given the time costs and direct costs of owning property, moreover, beating markets by 0.1% by year isn’t enough to mitigate for the costs

It is an illiquid asset – unlike REITS or index funds, you can’t easily sell direct real estate. That also makes you vulnerable to tax changes – you can’t simply sell your property if a new radical government comes to power

There has been a populist backlash – previously one of the biggest positives about property has been that it has been tax advantageous in most countries and you can use real estate investments to get second residencies and even passports. So many investors could “kill two birds with one stone” by getting an overseas residency and property. That is still possible in some places, but it is much harder than before, with many countries closing schemes or raising requirements. Likewise, many of the tax advantages of property have been closed down in numerous countries. If we take the UK as an example, the British Government has dramatically increased taxes on second homeowners.

The tax rules and general rules are always changing – it seems with ever budget, brings a new tax or change. The direction of travel seems to be towards more tax and regulation.

High valuations or high risk – most markets are either very risky or have high valuations. Some of the cheap emerging market opportunities, like in Georgia, are risky. Some of the safer options, are overvlaued.

For those that do want direct property, how easy is it to get mortgages for expats?

Over the years, it has gotten harder for expats, and indeed foreign buyers, to get mortgages.

In the UK, Australia and countless European markets, most lenders perceive expats as higher risk than people living locally.

That is because many expats are earning in foreign currency, and are on 2-3 year contracts, or are self-employed.

So you can get a UK mortgage as a non-resident, but the process is often more time-consuming, and you often have to put down a bigger deposit on day 1, compared to people living locally.

Where can I go for expat mortgages?

Many online websites have expat mortgage calculators, which show that the interest rates are typically higher for expats.

Some of the most famous banks, including HSBC expat, offer buy-to-let mortgages to UK and other expats, but the exchange rates aren’t always competitive.

This can also be an issue for people living in the UK, and other countries, that have overseas income.

There are countless British people, and indeed foreign-nationals, living in the UK, who have overseas income and are paid in Euros and USD.

Beyond the UK, countless countries such as Australia and especially New Zealand, have put restrictions on overseas property buyers, after a backlash against rising property prices.

What are some of the cheapest property markets right now?

Some up-and-coming markets include Georgia and Bulgaria, in Europe. Beyond that, many parts of the UK are increasingly being seen as cheaper than comparative markets.

With the whole “Northern Powerhouse” project, countless people are seeing Manchester, Liverpool and other parts of the North of England, as good options for real estate.

Typically speaking, the North and Midlands have better property yields, than London and the South East.

How about property tax?

This depends on the country again. If we tax the UK as an example again, there is a buying tax, called stamp duty. This ranges from 0% on cheaper houses, through to 12% on houses worth over 1.5M Pounds.

People who are buying property as a second home, have to pay an additional 3%, meaning an effective rate of 3%-15%.

It isn’t hard to negate this fee, although you can sometimes transfer a property’s deeds as a gift or put it in a will.

In addition to that, any income from property, will also be included towards UK Income Tax.

Below 11,851GBP a year, you don’t have to pay UK income tax. Above this threshold, and until 46,350GBP, a 20% rate is applied.

Above 46,350GBP, a 40% rate is applied. So people with multiple properties in the UK, often face an income tax increase, regardless of where they live, and they also face the hassles of needing to self-assess their own taxes.

Finally, you have capital gains tax. This didn’t used to apply to non-residents, including British expats and foreign buyers, but it now does.

You are generally taxed at 18%-28%, depending on many factors. Trusts are taxed at 28%.

The point is, property isn’t always tax advantageous. It can be high-tax, in certain situations, and the rules are complex and ever-changing.

Can you easily reduce your tax bil on direct property?

There are ways you can use deductions to reduce your tax bill. Expenses from insurance and maintenance bills are just two examples of allowable expenses.

These rules are always changing, and indeed the UK Government is currently making changes to the mortgage interest cost element of allowable expenses.

One of the advantages of loan notes and REITS, is that they can be put into more tax efficient structures – sometimes even 0% rate structures.

How about for Americans and Australians?

Americans need to pay tax on overseas income beyond a certain threshold and need to declare any overseas assets, even if the threshold has not been breached.

This is regardless of whether the investment is in direct real estate, REITs or any other kind of investment.

For Australians, expat mortgages are possible to get, but like for Brits, tend to be a bit harder than for local residents.

Do you advise on real estate?

My specialism is portfolios which compromise of stocks, bonds and something REITS and loan notes, as opposed to direct real estate.

My portfolio minimums are $75,000, or currency equivalent, for such services.

I can take clients from everywhere in the world, except those living in the US. American expats are sometimes OK, but investment options can be more limited, due to US tax rules.

However, I do have access to several property companies, if my clients ask for an introduction.

Typically, they have a specialism, such as expat mortgages and property. The majority of them are focusing on the UK, Australian, Canadian, US and Hong Kong Markets.

A few do have access to some emerging markets, such as Bulgaria.

Speaking to expat clients for about a decade now, most are confused about investing options whilst living overseas.

They hear contrasting information from different sources, about property, stocks, pensions and other investment choices. Worries about tax are also common.

This article will try to speak about some of the investing options for expats, in a clear and straight forward manner.

Needless to say, I can’t review the situation for around 200 countries and nationalities, but will focus on the key points and commonalities.

I will also answer some of the most frequently asked questions and make some concluding remarks.

What are the most frequently sold expat policies?

Savingsplans and offshore bonds, are widely sold to expats. These policies are usually administered from British Overseas Territory such as Isle of Man, Bermuda, Cayman Islands and British Virgin Islands, although some are administered from places such as Ireland and Luxembourg.

These policies are especially widely sold in high density expat cities like Qater, Dubai, Hong Kong, Saudi Arabia and Singapore, but they are sold in over 150 countries globally.

Whilst there are often benefits to such plans, including significant tax advantages for British and Australian expats, many of these expat plans are expensive.

I have reviewed these plans before, so I won’t go into too much detail here. Essentially, the main issue is that these plans are good value if, and only if, you keep contributing into them for the whole term of the investment.

So a 10-year saving plan, as an example, is cheap if you contribute for the whole 120 months. If you fail to contribute for a few months, the plans become more expensive, due to the extra fees levied by the providers.

What are some of the good alternatives to these traditional expat investments?

Many platforms and newer life insurance and banking firms, charge much more reasonable fees, whilst maintaining the tax benefits of the traditional expat plans.

This is especially the case for online firms, that have cut out many of the traditional costs, associated with financial services.

This brings with it significant advantages. Over a 10-year life cycle, a cheaper policy may save you tens, or even hundreds of thousands of pounds.

This will improve the net performance of your investments.

How about local investment solutions?

In a small number of places, local solutions make sense. For example, expats living in the United States should usually consider local solutions, for tax reasons.

In general, however, expats are moving from country to country every 3-5 years. Or even if they are not, they often want to return home eventually.

So local-solutions often don’t make sense for a number of reasons. Firstly, some local solutions aren’t very tax-efficient for expats.

Second, many expats I know are cashing in their policies, every time they move. This isn’t tax or cost-efficient, as capital gains tax applies every time you sell.

There is also the issue of investor protections. Many countries don’t have the sorts of investor protections that many offshore jurisdictions provide, such as Luxembourg, Isle of Man, British Virgin Islands and Bermuda.

Such locations usually have British Government protection (90% deposits protection in the case of Isle of Man), or the segregated accounts system, which negates the need for a guarantee.

Currency can be another issue. I have met countless expats who save and invest in the local currency, only to see a sharp devaluation relative to the USD.

This can happen even in unexpected situations. 10 years ago, most expats in China were interested in local solutions, as they were convinced the RMB would keep rising against the USD.

Subsequently, the RMB has moved from 6:1 to about 7:1 against the USD, and the local stock market has underperformed relative to the USD.

What are the biggest financial mistakes you have seen expats make overseas?

Familiarity-bias is a huge issue. It is human nature to be reassured by investments that others close to you are making, even if you would never have considered that option a few years ago.

Very few expats, as an example, are interested in local property or land on day 1 of their expat adventure.

Over time, after listening to talk of huge returns at dinner parties, many expats get seduced by the chance to get rich quick.

Whilst this can sometimes work, we have to remember that property is a complex legal product, and it isn’t liquid.

Meaning that you can’t just sell it easily. This is an even bigger issue with land investments. In 2014, I met two expats, in Indonesia and Cambodia, that boasted to me about their returns.

Subsequently, they couldn’t sell their land (the expat in Cambodia) or apartment (the expat in Indonesia) for various reasons.

A gain isn’t a gain until you sell, and most developing countries don’t have the sorts of legal systems that we have back home.

Are the big expat banks some of the best options?

Speaking about familiarity, some expats are reassured by familiar-sounding banking names. In general, the bigger banks take advantage of their brand name and charge high fees. Moreover, they aren’t independent.

In practice, this means they will have a limited number of funds available. For example, HSBC Expat is likely to sell HSBC funds, and offer limited solutions, as opposed to cheaper alternatives.

In general, banks are best for banking solutions, and platforms are best for investments. It might seem convenient to have everything under the same roof, but it is usually expensive.

How about expat taxes on investments?

Expat taxes are incredibly complex areas, as it depends on your nationality and where you live. I am not a tax advisor, but I will try to summarize here.

As a generalization, for American expats, it makes sense to invest with a broker back at home. This is unless an expat brokerage firm has a product specific to US expats.

For expats living in America, meaning non-Americans living in the US, it can also make sense to contact a US broker.

For most nationalities, however, investing offshore whilst living overseas, makes the most sense. Sending money home can cause tax issues, as can only focusing on local solutions.

This is especially the case if you need to move cities/countries every 2-5 years, meaning your liquidate your investments every time you move.

As capital gains taxes apply when you sell an investment, it is preferable to focus on long-term expat investing.

For British expats, in particular, portfolio bonds can have significant tax advantages, but it does depend on the charging structure chosen.

What about ISAs and other forms of tax-efficient investing?

Most onshore tax-free investment options like ISAs for British people aren’t available for expats unless it is just a short-term assignment.,

If you are spending less than 6 months a year overseas, however, the situation can be a bit different, as your tax residency may be in your home country.